This stock market is like the old line about having one foot in a bucket of scalding water and the other in a bucket of ice, netting out to a neutral, if not comfortable, temperature.

There’s the blistering Nasdaq, with its unassailable technology gatekeepers and a combustible frenzy in Tesla stealing much of the market’s oxygen. Then there’s the chill enveloping smaller stocks, vestiges of the physical consumer economy and legacy financial institutions.

Together they have the inclusive S&P 500 in a tight and tidy trading range, last week refusing plenty of excuses to break down, finishing at a one-month high and even showing signs of giving the benchwarmer value stocks a chance to play with Friday’s broader rally.

The crucial question swirling around the Nasdaq’s ascent and refusal of the Big Six stocks to take anything but a quick rest for months is whether investors are in danger of overpaying for the perceived certainty of secure cash flows, durable growth and entrenched franchises in the digital economy.

There is no denying both that the Nasdaq complex in the short-term appears technically stretched and over-loved, while large-cap tech is getting richly valued.

Over-loved tech?

SentimenTrader.com notes that about three-quarters of Nasdaq stocks are above their 200-day moving average, the shorthand definition of a longer-term uptrend, while only about 40% of S&P 500 names are in that position. This gap in breadth is either rare or unprecedented:

The Nasdaq 100 has pushed more than 22% above its 200-day average, according to Baycrest Partners’ Jonathan Krinsky, the most extreme spread with the index at a high since 2000.

And the S&P tech sector has returned to its peak price-to-sales ratio from the March 2000 tech-bubble market top.

Source: FactSet

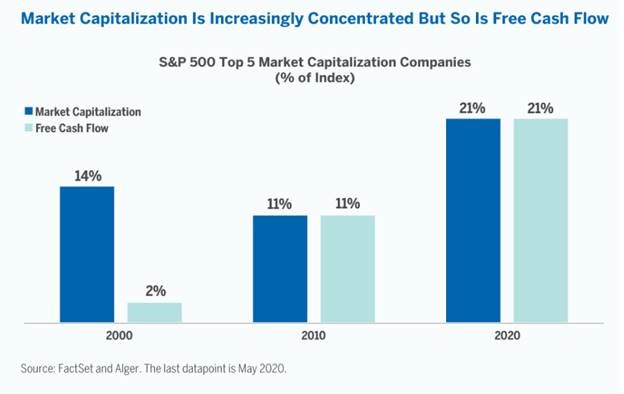

For sure, today’s tech companies are more profitable than those of two decades ago. And while the five largest S&P 500 stocks are all from the Nasdaq and in the tech or Internet realms (Apple, Microsoft, Amazon, Alphabet and Facebook) now make up a 20-year high 21% of the S&P 500, they also kick in a commensurate portion of the index’s free cash flow, as this breakdown from Fred Alger Management shows.

And as wild as the Nasdaq’s surge and outperformance have been, it simply hasn’t piled up the amount of easy riches that it had in the late-’90s run. In the five and ten years through the end of 1999, the Nasdaq Composite had gained 440% and 800%, respectively. The comparable gains over the past five and ten years: up 111% and 380%.

Admittedly, arguing that the current market is not as expensive, frothy or beloved as the most overvalued, overextended and overestimated market in many decades is not exactly a ringing endorsement. And indeed we may never see a close rerun of that period. But, as argued here a few weeks ago, stocks can be stoutly valued and priced for subpar future returns without representing an unstable bubble or dangerous misallocation of capital.

Another qualitative distinction between today’s outsized Nasdaq contribution to the market’s climb and the one that culminated 20 years and four months ago: The crowding into the mega-cap elite names today is a defensive instinct, investors gravitating toward steadiness and predictability rather than blue-sky hopes of galloping growth rates and innovative disruption to come. As long as corporate-debt yields remain so low and cash-flow streams are seen as very scarce, what might upend this part of the market beyond nasty short-term corrections and shakeouts.

Missing the Wall Street hype

Back in the late ’90s, the market was implicitly over-extrapolating massive growth rates for many years in companies more cyclical than appreciated, such as Cisco Systems and Intel (along with Microsoft, Oracle, Yahoo and other graybeards of Silicon Valley).

There is an unusual situation now in which the tech darlings have been barreling higher largely on macro fears and heavy liquidity flows rather than product hype or Wall Street salesmanship. In fact, the consensus analyst price targets for Apple, Microsoft and Amazon are all below the stocks’ current quote, according to FactSet.

Does this show a helpfully cautious analytical corps serially underestimating today’s best companies — a sturdy wall of worry built by Wall Street itself? Or is it a sign the market has carried them beyond even the sell side’s typically rosy calculus of fundamental value?

Who knows, Friday’s mean-reversion action, with banks, energy and small caps retaking a sliver of the territory dominated by tech, is the start of a rebalancing of the market. The levitation in secular-growth sectors has arguably been the market’s way of deploying ample liquidity to stay supported as the country backslides on Covid containment and the economy fitfully tries to recover.

It’s tough to deny that big chunks of the Nasdaq are in the sway of overheated speculation. Tesla, to take the obvious example, has gained $108 billion in market value in two weeks. More than $34 billion worth of the stock traded on Friday alone, twice the turnover that day in Amazon – a company whose market cap is more than five times as large.

This is fevered, heedless action, feeding on itself and punishing the disciplined. And the more it goes on or spreads to other stocks, the harder it will become to make the case that this is a market unappreciated by a skeptical investing public.

CNBC / Balkantimes.press

Napomena o autorskim pravima: Dozvoljeno preuzimanje sadržaja isključivo uz navođenje linka prema stranici našeg portala sa koje je sadržaj preuzet. Stavovi izraženi u ovom tekstu autorovi su i ne odražavaju nužno uredničku politiku The Balkantimes Press.

Copyright Notice: It is allowed to download the content only by providing a link to the page of our portal from which the content was downloaded. The views expressed in this text are those of the authors and do not necessarily reflect the editorial policies of The Balkantimes Press.